Automotive businesses live in a world of mixed ticket sizes, unpredictable parts availability, delayed fulfillment, and customers who want to pay now—whether they’re standing at the counter, approving an estimate by phone, or clicking an online invoice.

That reality makes payment processing more nuanced than in many other industries, and it’s exactly why automotive merchant account fees can look confusing (and sometimes surprisingly expensive) when you first review a statement.

This guide breaks down automotive merchant account fees in plain language—what you’re actually paying for, which charges are avoidable, and how pricing structures differ for repair shops, mobile mechanics, tire and lube centers, collision facilities, towing operators, parts retailers, and vehicle sellers that accept card payments.

You’ll also learn how underwriting and risk controls influence automotive merchant account fees, what “effective rate” really means, and how to reduce costs without putting approvals, funding, or customer experience at risk.

Throughout this article, you’ll see the phrase automotive merchant account fees often because that’s the topic—but you’ll also see closely related terms that matter for ranking and real-world understanding: interchange, assessments, processor markup, card-present, keyed-in, AVS, chargebacks, PCI compliance, surcharge rules, cash discounting, reserves, and funding schedules.

What an automotive merchant account is and why pricing differs

A merchant account is the payment “plumbing” that allows your business to accept card and digital wallet payments and deposit proceeds into your bank account.

In automotive, that account is usually paired with a POS system (countertop or tablet), a payment gateway (for online invoices), and sometimes a virtual terminal (for keyed-in or phone payments). The result is a stack of moving parts—and each part can influence automotive merchant account fees.

Automotive pricing differs from general retail for three big reasons. First, transaction patterns can be irregular: one customer might pay $49.99 for wipers, another might approve a $2,400 brake and suspension job, and a third might pay a deposit today and the balance next week.

Second, fulfillment timing varies. When work is performed after authorization (diagnostics, special-order parts, multi-day repairs), processors and card networks view the transaction as higher risk than a simple “grab-and-go” retail sale.

Third, disputes are more common than many merchants expect. Customers may claim the repair didn’t fix the issue, allege the final amount differs from the estimate, or dispute a card-not-present invoice.

Because of these risk and operational realities, underwriting standards can be stricter, and cost controls like reserves (or delayed funding) are more common—both of which affect automotive merchant account fees either directly (reserve requirements) or indirectly (higher markups).

Automotive vs general retail risk factors

Risk is a pricing lever. Even if two businesses run the same card brands through the same network rails, the processor’s margin and underwriting posture can differ.

Automotive merchants often face higher risk flags: higher average tickets, more keyed-in transactions (especially for phone approvals), more returns and partial credits, and more “service-not-as-described” disputes.

That doesn’t mean automotive merchant account fees must be high. It means your pricing will be strongly influenced by how you take payments and how well your documentation supports the transaction.

Clean estimates, signed authorizations, clear invoices, consistent refund policies, and the right transaction types (e.g., using “delayed capture” or “estimated/adjusted” only when appropriate) can reduce dispute exposure—and that can translate into better approvals, fewer holds, and often more competitive automotive merchant account fees over time.

The full fee stack: interchange, assessments, and processor markup

To understand automotive merchant account fees, you need to separate the fee stack into three layers:

- Interchange: The base rate paid to the cardholder’s issuing bank (the bank that issued the customer’s card). This is typically expressed as a percentage plus a per-transaction fee.

Interchange varies based on card type (debit/credit, rewards, commercial), how the transaction is processed (chip/tap vs keyed-in), and data quality (address verification, additional data fields, etc.). - Assessments and network fees: Fees collected by the card networks (and sometimes additional network-related pass-through charges). These are smaller than interchange but still meaningful at scale.

- Processor markup: The provider’s margin and account-level fees. This is the part you can negotiate most directly.

In other words, most of what you pay in automotive merchant account fees is not purely “profit” to your processor. A large share is interchange and network costs that exist regardless of which provider you use.

Your goal is to minimize avoidable downgrades, reduce risk-driven markups, and choose a pricing model that doesn’t quietly inflate your bill.

Interchange basics and why recent updates matter

Interchange tables are periodically updated. Mastercard publishes regional interchange programs and rate documents that outline categories and qualifications for different transaction types.

Similarly, research and summaries from the Federal Reserve–related sources show how debit network fee schedules and interchange structures can vary, particularly where “premium issuer” or network-specific constructs exist.

What this means in practice: small changes in how you run a transaction can move it into a different interchange bucket. For automotive businesses, common triggers include:

- Keyed-in vs chip/tap

- Storing a card on file and charging later (credential-on-file rules)

- Invoice links (e-commerce style processing) vs in-person capture

- Missing AVS or incomplete billing data on keyed transactions

- Splitting a ticket into deposit + balance incorrectly

If you’re trying to reduce automotive merchant account fees, the best starting point isn’t “negotiate harder.” It’s ensuring your transactions qualify for the best possible buckets given your real workflow.

Common automotive merchant account fee types you’ll see on statements

Most statements mix a few categories of automotive merchant account fees. Some are legitimate pass-through costs; others are optional add-ons or “junk fee” style charges that can often be removed.

Transaction-based fees typically include:

- Discount rate or interchange + markup (percentage)

- Per-transaction fee (cents per sale)

- Authorization fee (sometimes separate from the transaction fee)

- AVS fee (common for keyed/online transactions)

- Batch fee (daily or per settlement batch)

Monthly account fees might include:

- Monthly minimum (you pay the difference if you don’t hit a certain fee threshold)

- Statement fee

- PCI program fee (or non-compliance fee if you don’t validate)

- Gateway fee (for invoice links, online checkout, or integrations)

- POS software subscription (sometimes billed separately)

Incidental and risk-related fees can include:

- Chargeback fees

- Retrieval/request fees (when a customer requests documentation)

- NSF/returned payment fees (for ACH programs)

- Reserve or rolling hold (not always a fee, but impacts cash flow)

Your job is to identify which automotive merchant account fees are:

- Unavoidable (interchange/assessments)

- Negotiate-able (processor markup, monthly fees)

- Behavior-driven (downgrades, chargebacks, keyed-in risk)

- Optional (certain add-ons and “protection plans”)

Monthly and annual account fees: what’s normal vs padded

A fair merchant account can have a small number of fixed fees, especially if you’re using a gateway, invoicing tools, or advanced reporting. But automotive merchant account fees often get inflated by stacked charges: a “platform fee,” “account fee,” “statement fee,” “non-PCI fee,” “regulatory fee,” and more—some of which overlap.

A common red flag is paying multiple fees for the same underlying service: for example, a gateway fee plus a separate “online reporting” fee plus a “security” fee that isn’t tied to actual security tooling.

Another red flag is a monthly minimum that triggers frequently even when your sales are steady. If a provider uses a monthly minimum, it should be transparent, reasonable, and paired with competitive markup.

For automotive merchants, the cleanest path is usually:

- One transparent pricing model (often interchange-plus)

- A short list of fixed fees tied to real services you use

- No surprise annual “membership” charges unless the value is clear

- A PCI process that’s simple enough that you actually complete it—so you don’t pay avoidable penalties

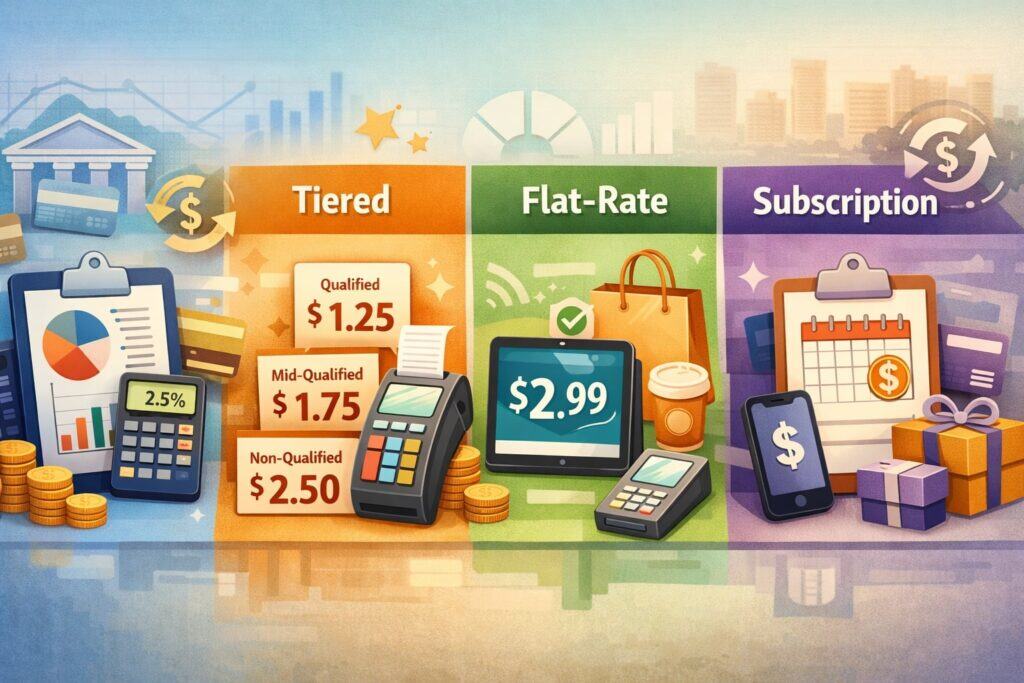

Pricing models compared: interchange-plus, tiered, flat-rate, and subscription

Automotive merchant account fees depend heavily on your pricing model. Two businesses can process the same volume and pay very different totals because the model determines how costs are bundled and disclosed.

- Interchange-plus: You pay interchange + network fees (pass-through) plus a fixed markup (e.g., 0.30% + $0.10). This is often the most transparent model and typically the easiest to audit. If your operation has a lot of card-present volume and decent data quality, interchange-plus can be cost-efficient.

- Tiered pricing: Transactions are grouped into “qualified,” “mid-qualified,” and “non-qualified” tiers. This model often looks simple but can be expensive because many automotive scenarios (keyed-in, invoice links, rewards cards) end up in higher tiers.

Tiered pricing is where automotive merchant account fees can quietly balloon, especially when the statement doesn’t show what drove a transaction into a higher tier. - Flat-rate: A single rate for most transactions (like 2.6% + $0.10 style pricing). Flat-rate can be convenient for startups or very small volumes, but it often becomes expensive as volume grows—especially for automotive businesses with higher tickets.

- Subscription/membership: You pay a monthly fee and then a small per-transaction markup (sometimes just cents). This can reduce automotive merchant account fees for higher-volume merchants, but only if the provider is reputable and the pass-through costs are handled correctly.

Which model fits repair shops, dealerships, and parts sellers

Repair shops and service-heavy businesses often do best with interchange-plus when they can keep most payments card-present and maintain clean documentation. Parts sellers with retail-style flow can also benefit from interchange-plus due to predictable, card-present behavior.

Businesses with frequent keyed-in approvals (phone authorizations), remote invoicing, or higher dispute exposure may still use interchange-plus successfully—but they need tighter operational controls to avoid downgrades and chargebacks, which is where automotive merchant account fees can spike.

For vehicle sellers that take deposits, the biggest risk is running transactions in ways that look like “future delivery” without proper indicators or documentation.

In that environment, subscription models can work, but only when the provider has strong underwriting alignment with your sales process and doesn’t introduce funding delays that disrupt customer delivery schedules.

Card-present vs card-not-present in automotive: POS, invoices, phone orders, and online

How you accept payments is one of the fastest ways to change automotive merchant account fees without changing providers. Card-present transactions—chip and contactless—tend to price better and dispute less.

Card-not-present transactions—keyed-in, invoice links, online checkout—carry higher fraud and dispute risk, and they often trigger additional pass-through fees such as AVS.

Automotive businesses commonly mix modes:

- Customer at the counter: chip/tap

- Customer approves work by phone: keyed-in virtual terminal

- Customer pays after-hours: text/email invoice link

- Fleet accounts: stored credentials and recurring billing

- Mobile mechanic: tap-to-pay on phone or portable terminal

Each mode has a best-practice configuration. For example, if you do invoice links, ensure the invoice includes clear line items, shop contact info, cancellation/refund language, and an authorization statement.

If you do phone approvals, always capture AVS and match billing ZIP when possible. These steps won’t eliminate automotive merchant account fees, but they reduce the risk-driven costs that show up as higher markups, more holds, or more chargebacks.

How authorization, AVS, and adjustments affect fees

Automotive transactions often involve estimates and changes—diagnostic fees, added parts, additional labor. Some businesses authorize one amount and then “adjust” it at capture. If handled incorrectly, this can increase disputes or cause processing qualification issues.

AVS is especially important for keyed-in and invoice transactions. It helps validate the billing address information and can reduce fraud. Many providers charge a small AVS fee, but it’s often worth it because the alternative is higher chargeback exposure and more expensive automotive merchant account fees in the long run.

Another detail: partial approvals and split tenders can occur when customers use debit with limited funds or want to split across cards. Your POS should support this cleanly, because awkward workarounds (multiple voids, re-runs, manual entries) create reconciliation errors and increase operational risk—both of which can affect your account standing and future pricing.

Risk controls that impact cost: chargebacks, fraud, reserves, and underwriting

A payment provider’s underwriting team cares about one question: “Will this merchant create losses?” If the answer looks uncertain, your automotive merchant account fees rise via higher markup, stricter limits, rolling reserves, delayed funding, or extra monitoring.

Automotive merchants can trigger risk flags when they have:

- High average tickets with inconsistent sales patterns

- High keyed-in or card-not-present volume

- High refund ratios

- Poor descriptor clarity (customers don’t recognize the charge)

- Weak documentation on estimates and authorizations

- Multiple locations using mismatched merchant descriptors

Chargebacks are the biggest driver. Each dispute costs you the sale amount plus fees and labor. A pattern of disputes can also push you into a higher risk tier internally, increasing automotive merchant account fees even if your sales volume grows.

Reserves are another lever. A rolling reserve isn’t always a “fee,” but it is a cost because it ties up cash flow. If your shop depends on daily funding to buy parts, a reserve can be painful. The best way to avoid reserves is to demonstrate operational maturity: stable history, consistent documentation, low dispute rates, and clean settlement behavior.

How to reduce chargebacks in auto services

Chargebacks in automotive often come from misunderstanding and timing, not fraud. The most effective fixes are procedural:

- Use clear estimates with customer sign-off (digital signatures count when implemented properly).

- Send “work authorized” confirmations for phone approvals.

- Itemize invoices with parts, labor, shop supplies, and taxes clearly separated.

- Use a recognizable statement descriptor (shop name, phone number).

- Set expectations about diagnostics: what the fee covers and what it doesn’t.

- Make refunds predictable: publish the policy and follow it consistently.

When customers recognize the charge and understand what they approved, disputes fall. When disputes fall, providers see you as lower risk. Over time, that improves stability, reduces holds, and can lead to better automotive merchant account fees because the processor doesn’t need as much margin to cover risk.

Compliance and rules: PCI, surcharging, cash discounting, and receipts

Compliance influences automotive merchant account fees because non-compliance creates cost, risk, and penalties. The most common compliance driver is PCI DSS. Even if you never store card numbers, you still have responsibilities: maintaining secure devices, using compliant software, and validating annually via the appropriate questionnaire.

The second major driver is pricing transparency and card brand rules around surcharging. Many automotive merchants consider surcharging when margins feel squeezed. But surcharging is not “set it and forget it.”

It has network rules, notice requirements, disclosure expectations, and in some places additional state-level conditions. A state-by-state surcharging guide can help identify caps and disclosure requirements that differ by location.

Your own compliance approach should also reflect current card brand guidance and practical merchant implementation considerations.

If you violate surcharge rules (like surcharging debit, failing to disclose, or exceeding caps), you can face fines or processing consequences. Those consequences often show up as higher automotive merchant account fees later—or in worst cases, account termination.

State-level surcharge considerations and practical guardrails

Surcharging is governed by a combination of card network rules and state laws. Some states allow it with minimal additional constraints; others impose special disclosure formatting or caps that can override broader network limits.

If you decide to surcharge:

- Use compliant signage at the point of entry and point of sale.

- Ensure receipts show the surcharge amount clearly.

- Apply it only where allowed and only on eligible payment types.

- Keep the surcharge at or below the allowed cap and aligned to your actual cost.

- Notify networks as required and retain documentation.

If you want a simpler alternative, many automotive merchants use a cash discount program (advertise a “cash price” and a higher card price). But cash discounting also has rules and must be implemented cleanly to avoid customer complaints, which can ironically increase disputes—raising automotive merchant account fees in a different way.

How to audit and lower automotive merchant account fees

Reducing automotive merchant account fees starts with measurement. Most merchants look at one number—“my rate”—and miss the real levers. You want to calculate:

- Effective rate = total fees / total sales volume

- Cost per transaction = total fees / number of transactions

- Card-present mix = percentage of volume that is chip/tap

- Keyed-in and invoice mix = higher risk portion of volume

- Chargeback ratio = disputes / transactions (and by dollar volume)

Then you compare those metrics to your operational reality. If your keyed-in volume is high because you take phone payments, your focus should be: better invoice links, tap-to-pay for remote capture, or collecting deposits in-person where possible.

If your effective rate is high because your ticket size is small, then per-transaction fees matter more than percentages—and you negotiate differently.

You also want to audit for fee clutter:

- Are you paying for services you don’t use?

- Are you paying multiple “security” or “compliance” fees?

- Are you paying a monthly minimum despite consistent volume?

- Are there “non-qualified” surcharges that indicate tiered pricing pain?

A clean audit usually finds savings through a combination of operational tweaks and pricing simplification, not just a lower headline rate.

Statement math that actually reveals the truth

Processors can make automotive merchant account fees look low by advertising a single attractive rate. The statement tells the truth, but only if you read it correctly. Look for:

- Markup shown separately from interchange (good sign of transparency)

- A breakdown by card type and entry mode (chip vs keyed)

- Network and pass-through fees identified clearly

- Chargeback and retrieval fees listed explicitly

If you see lots of miscellaneous charges with vague names, that’s a sign to demand clarity. The best providers can explain every line item and show you which are pass-through costs vs their own markup.

When you can separate those, you can negotiate effectively—and you can compare offers without getting trapped by misleading “as low as” pricing that doesn’t match automotive workflows.

Future predictions: where fees and payments are heading for automotive businesses

Automotive payments are moving toward faster funding, more embedded financing options, and more digital-first customer experiences—especially for service approvals and post-repair payments.

That evolution can reduce friction, but it can also increase card-not-present volume, which may push automotive merchant account fees upward unless merchants adopt stronger verification and documentation.

Several trends are likely to shape costs:

- More customers will prefer invoice links, text-to-pay, and online portals.

- Tap-to-pay on phone will expand for mobile service and pickup/drop-off workflows.

- Real-time account-to-account options may grow in use for high-ticket invoices, especially for fleets.

- Processors will continue tightening risk models around disputes and “delayed fulfillment” services.

Another major factor is merchant pressure on interchange and network rules. A recently reported settlement framework between major card networks and merchants has been discussed as offering modest average interchange reductions over time, while still requiring approval and facing criticism from some trade groups.

Whether those specific terms hold or change, the direction is clear: merchants want more routing choice, more transparency, and more competition—all of which could reshape future automotive merchant account fees.

What to watch next in interchange and regulation

From an operator’s standpoint, don’t build your 2026–2028 plan on “fees will drop.” Instead, plan on:

- Continued complexity in fee structures

- Ongoing emphasis on transparency

- More compliance obligations for digital-first payments

- Greater differentiation between merchants who document well and those who don’t

The shops that win will be the ones who treat payments like a process: consistent estimates, clean authorizations, recognizable descriptors, and payment methods aligned to the job’s lifecycle.

That approach reduces disputes and makes you “low risk” in the language of underwriters—which remains one of the most reliable paths to stable, competitive automotive merchant account fees.

FAQs

Q.1: What are typical automotive merchant account fees for a repair shop?

Answer: Typical automotive merchant account fees depend on your mix of card-present vs keyed-in transactions, average ticket size, monthly volume, and dispute history.

A repair shop that runs most payments via chip/tap at the counter and has low chargebacks usually lands in a more efficient cost profile than a shop that keys many payments, sends invoice links for most jobs, or frequently issues refunds.

It’s also important to distinguish between rate and total cost. A shop with many small tickets might pay more in per-transaction fees even if the percentage rate looks fine. Meanwhile, a shop with larger tickets may care more about basis points (small differences in percentage) because they multiply across higher dollars.

The most accurate way to judge your automotive merchant account fees is to compute the effective rate over 2–3 months and then break that down by entry mode.

If your effective rate is high, the fix might not be “find a cheaper processor.” It might be “reduce keyed-in volume,” “improve AVS usage,” “remove unnecessary monthly add-ons,” or “switch from tiered to interchange-plus” so your costs stop inflating behind the scenes.

Q.2: Why do keyed-in payments cost more for automotive businesses?

Answer: Keyed-in payments are treated as higher risk because the card isn’t physically present, which increases fraud potential and disputes.

That risk gets priced into automotive merchant account fees through higher interchange categories (in many cases), added verification costs like AVS, and sometimes higher processor markup due to increased chargeback exposure.

In automotive, keyed-in happens frequently because customers approve repairs by phone, fleet managers pay remotely, or the customer isn’t on-site when the vehicle is ready. The goal isn’t to eliminate keyed-in entirely—it’s to use safer alternatives when possible.

Text-to-pay invoice links, secure payment portals, and tap-to-pay on the phone can reduce manual entry. When you must key in, capture AVS and keep documentation strong: estimate approvals, authorization logs, and detailed invoices. Lower disputes and cleaner verification are two of the best long-term ways to stabilize automotive merchant account fees.

Q.3: Can I add a credit card surcharge to cover automotive merchant account fees?

Answer: Sometimes, but it’s rule-heavy. Surcharging is governed by card network requirements and can be affected by state-level rules, including caps and disclosure formats. You typically need clear signage and receipt disclosures, you must avoid surcharging debit in most cases, and you may have to provide network notice.

Surcharging can reduce the net impact of automotive merchant account fees, but it can also raise customer friction. In automotive service, trust matters. If a surcharge surprises a customer at pickup, it can trigger complaints, refunds, and even disputes—ironically increasing the costs you were trying to offset.

If you pursue surcharging, implement it professionally: transparent communication, compliant configuration at the POS and invoice level, and a surcharge amount aligned to actual processing cost. Many shops prefer a “cash discount” approach instead, but that must also be implemented correctly to avoid confusion.

Q.4: What’s the fastest way to lower automotive merchant account fees without switching providers?

Answer: The fastest wins usually come from changing how you process transactions and removing unnecessary add-ons:

- Shift more volume to chip/tap (including mobile tap-to-pay where possible).

- Use invoice links with strong documentation and consistent policies.

- Reduce keyed-in volume where it’s avoidable.

- Ensure AVS is enabled and used correctly for card-not-present.

- Complete PCI validation to avoid non-compliance fees.

- Ask for a fee review and remove redundant monthly charges.

Then measure again. If your effective rate drops and disputes stay low, you may be able to negotiate better automotive merchant account fees with your current provider based on improved risk performance and cleaner processing data.

Switching providers can help, but operational improvements often deliver savings immediately—and they make any future negotiation or provider change far more successful.

Conclusion

Automotive merchant account fees aren’t random. They’re the result of a layered pricing stack (interchange, network costs, and processor markup) combined with the specific risks and workflows common in automotive businesses.

When you understand what drives each cost—entry mode, data quality, disputes, refund behavior, and underwriting posture—you can reduce automotive merchant account fees in a way that doesn’t sacrifice approvals, funding speed, or customer experience.

The most reliable path is a two-step approach: first, optimize operations (more card-present volume, cleaner invoices, better verifications, fewer chargebacks). Second, align pricing (prefer transparent models like interchange-plus, remove fee clutter, and negotiate markup based on stable performance).

Do those consistently, and automotive merchant account fees become predictable, explainable, and manageable—now and as the payments landscape continues shifting toward more digital automotive customer journeys.